Outbound Investment from Vietnam

Quick Reference

For a long time, the easier direction of capital has been into Vietnam. Moving capital the other way, from a Vietnam company to a project abroad, has been harder.

That is now changing. Vietnam is slowly opening the door for its companies to invest overseas, but it is doing so under supervision. For business leaders, this is no longer just about getting documents prepared and signed off. It is a bigger question of long-term and visionary planning, with coordination across different functions within the company and the group, and corporate compliance maintained from set-up through ongoing operations in a way that can survive an audit.

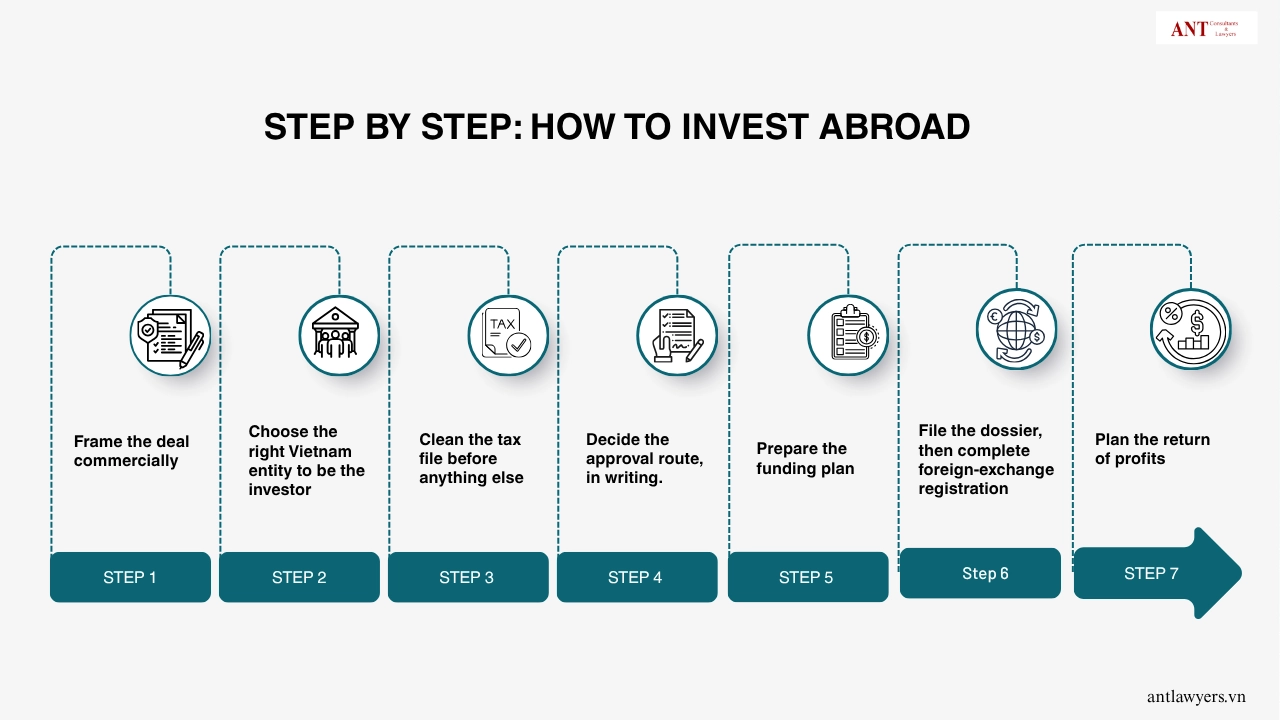

Here are seven rules that decide whether an overseas investment goes smoothly or runs into challenges along the way.

For most of the last two decades, the Vietnam growth story has been about money coming in. Now, more Vietnam-based companies, both purely Vietnamese groups and foreign-invested companies that use Vietnam as a regional base, want to invest overseas to buy shares abroad, open subsidiaries in neighbouring countries and beyond, hold intellectual property abroad, secure supply chains across borders, or build a wider regional structure.

Vietnam has noticed the same trend. Outbound investment is no longer treated as a side issue inside the broader investment rules. It now has its own dedicated legal framework, with its own logic and its own controls. That shift alone is a signal that the State sees this as an important topic in its own right.

The policy direction is to allow Vietnam-based companies to expand internationally, but through a structured system, with the right entity, the right account, and the right records. So outbound investment from Vietnam is no longer just talked about in theory. It is being planned and executed. The next question for business leaders is how to structure each move so that it makes commercial sense, the money can actually move through the bank, and the deal stays compliant from start to finish.

Many business leaders focus first on the project and the financial side, and only bring in legal review later. That used to be workable. It is much less workable now.

With outbound investment from Vietnam sitting in its own dedicated legal framework, the compliance side has become stricter and more sequenced. Legal, finance, and treasury have to move together, not one after the other. The legal opinion, the funding plan, and the banking workflow should be on the same table from the start. When any one of these does not match up, the deal usually slows down or fails at the bank counter.

The legal framework now sorts outbound projects into different categories. Small, low-risk projects do not carry the same procedural weight as large or sensitive ones.

Smaller projects in non-sensitive sectors can be handled at a lower approval level, or controlled only at the capital-transfer stage. Larger projects, and projects in sectors that Vietnam treats as sensitive, go through a fuller registration route at a higher level of government. Very large or strategically significant projects follow a separate route again.

For business leaders, the practical task is to plan the deal early, its capital amount, its sector, and its commercial purpose, and confirm which approval level applies. That answer shapes everything from how long approval takes, to what documents are needed, to how much attention the project will draw.

Even outbound projects at the lightest approval level must still pass through foreign-exchange registration with the central bank. And every cross-border flow related to the project, money going out, profits coming back, liquidation proceeds, must move through a dedicated outward investment capital account at a Vietnamese bank.

This is where the deal is checked and verified against the rules. The legal opinion confirms the structure, and then the bank starts asking different questions as part of its verification: where is the money coming from, what supports the purpose of transfer, is the tax position clean, was the project properly declared.

It is wise to prepare for these questions in advance and have proper records in place in the right form. In particular, the source-of-funds evidence should be ready, and the tax position cleaned up before the dossier moves.

Outbound investment does not have to be cash only. A Vietnam-based group may invest abroad by contributing intellectual property to a new subsidiary, by swapping shares in a cross-border acquisition, by using profits already retained overseas, by contributing machinery or technology, or by a combination of these.

The legal framework now recognises this commercial reality and allows a broader range of capital forms. That flexibility is genuinely useful for real deals.

But each form has its own document requirements. Cash needs clean banking records. Intellectual property needs a proper valuation. A share swap must be at market value and must not be used to manage tax. Whatever form is chosen, the value being transferred has to be proven clearly and on paper.

When a Vietnam-based company investing abroad is itself foreign-owned, the State applies stricter conditions. This is not about being harder on foreign investors; it is about an economic reality test. The State needs to be sure that the Vietnam company is a genuine business that earned its capital here and now wants to expand, rather than just acting as a “pass-through” to move money from one foreign country to another.

The policy goal is straightforward. Vietnam wants to encourage expansion by companies that have built real value locally. It also wants to prevent its territory from being used as a temporary transit point for capital that enters for one purpose and leaves for another. Most economies that manage capital flows apply a similar logic, and Vietnam is not unusual in doing so.

For business leaders, the impact is practical. A young, foreign-owned subsidiary that is not yet profitable cannot easily be turned into a regional holding platform without careful planning. A group hoping to push an acquisition through a brand-new Vietnam entity must prepare for extra scrutiny.

The good news is that once a company proves its economic reality, the rest of the outbound process is the same as for any other investor. The challenge is recognising early that this test applies and planning the deal around it. This is a structural question, not just a document requirement, and it should be addressed before a term sheet is signed.

When a Vietnam company invests abroad, its tax position in Vietnam is reviewed. Unresolved tax disputes, late filings, or open findings from a recent audit can stop an outbound application before it starts.

The fix is operational, not legal. The Vietnam tax file should be brought to a clean state in advance to avoid any doubts. For finance teams, this means treating tax housekeeping as part of the deal timeline, not as a separate task that runs in parallel.

One of the main goals is to stay compliant from start to finish. A compliant set-up makes it easier to bring profits back home smoothly, pass a tax review, or sell the business later without issues.

A non-compliant set-up leads to extra costs and delays. For example, a buyer might offer a lower price because the records are unclear; a bank might reject a profit transfer if the documents are wrong; or the tax authority might impose penalties because the document requirements were not met.

It is always less expensive to build the structure cleanly at the start than to fix a broken one later.

Decide what you are really doing. A subsidiary, a holding vehicle, a sourcing platform, an IP holder, or an acquisition, each implies a different structure, a different entity, and a different timeline.

Do not assume the company you already use is the right one. Test it against ownership, age, profitability, and the type of capital it can contribute. If the answer is in doubt, choose a different entity or reshape this one before moving forward.

Get the Vietnam tax position to a place where the tax authority can confirm it is clean. If there are open issues, fix them before you file. This step usually takes longer than expected.

Confirm which tier the project falls under. This determines which authority approves it, how long it takes, and what documents the dossier requires.

Identify the exact capital form, whether it is cash, retained earnings, IP, machinery, or a share swap, and the evidence each one needs. Open the dedicated outward investment capital account at a Vietnamese bank.

Once approvals are in place, register the foreign-exchange transactions with the State Bank of Vietnam (SBV), and only then begin remittance through the dedicated account.

From day one, set up a schedule for your required government reports (monthly, quarterly, and yearly). Establish a clear timeline for bringing profits back to Vietnam, and a system to keep all your records safe.

Q1: Is outbound investment from Vietnam allowed?

Yes. Vietnamese companies and Vietnam-based foreign-invested companies can invest abroad, subject to a supervised regime covering approvals, capital accounts, foreign exchange, and tax.

Q2: Does every overseas project need the same approval?

No. Smaller and low-risk projects travel through a lighter route. Larger or sensitive projects go through a fuller registration process.

Q3: Can a foreign-invested company in Vietnam invest abroad?

Yes, but under stricter conditions than a purely Vietnamese-owned company. The conditions are structural and should be reviewed before the deal is shaped.

Q4: Why does the bank ask so many questions about outbound investment?

Because cross-border flows must go through a dedicated capital account at a Vietnamese bank, and the bank is responsible for matching the legal file against the transaction.

Q5: What is the biggest mistake to avoid?

Treating outbound investment as a filing matter rather than a structural one. The deal is usually decided long before any form is filed.

Outbound investment from Vietnam is now a growth opportunity managed by a clear legal framework. Vietnam is making more room for companies, including foreign-invested companies based here, to expand internationally. It is doing so through a structured system, with differentiated approval paths, dedicated capital accounts, specific requirements for foreign-owned investors, and clearer expectations regarding tax and reporting discipline.

For business leaders who wish to invest abroad from Vietnam, the key question is how to structure that move so it is commercially useful, legally clean, bankable, and auditable.

We help clients overcome cultural barriers and achieve their strategic and financial outcomes, while ensuring the best interest protection, risk mitigation and regulatory compliance. ANT Lawyers has lawyers in Ho Chi Minh city, Hanoi, and Danang, and will help customers in doing business in Vietnam.

How ANT Lawyers Could Help Your Business?

You could reach ANT Lawyers for advice via email ant@antlawyers.vn or call our office at (+84) 24 730 86 529

The Vietnamese Government has issued Resolution No. 66.23/2026/NQ-CP, dated July 24, 2026, introducing temporary special…

On July 28, 2026, the Prime Minister issued Decision 1415/QĐ-TTg, which approves the National Program…

A construction payment dispute in Vietnam often becomes visible when a contractor submits a progress…

On July 27, 2026, The Vietnam Ministry of Industry and Trade (MOIT) issued Decision No.…

EPC contract review in Vietnam should happen before the foreign contractor signs, mobilizes people, or…

Malaysia has opened an anti-dumping investigation on aluminium zinc coated steel products originating in or…

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}